iShares Core S&P 500 UCITS ETF USD (Acc) (CSPX)

Новости по iShares Core S&P 500 UCITS ETF USD (Acc)

- От Investing.com

- • 05 окт. 2023 г. •

Investing.com — Аналитик Кэти Стоктон из Fairlead Strategies считает, что фондовый рынок в США уже готовится к восстановлению после сильной распродажи, так как 5 внутренних.

- От Investing.com

- • 03 окт. 2023 г.

Investing.com — Энтузиазм из-за потенциала ИИ в этом году помог фондовому рынку оправиться от резкого падения прошлого года. Несмотря на повышение ставки Федеральной резервной.

- От Investing.com

- • 03 окт. 2023 г. •

Investing.com — Акции крупнейших по своей капитализации технологических компаний, или иначе «Великолепной семерки» обеспечили большую часть роста индекса S&P 500 в этом году. В.

Аналитика по iShares Core S&P 500 UCITS ETF USD (Acc)

- От Андрей Цветков

- • 19 ч. назад

Аналитика по волнам Эллиотта по инструментам: Биткоин, Эфир, РТС, ММВБ, Сбербанк (MCX:SBER), Японская Йена, Евро, Индекс доллара, Австралийский доллар, Новозеландский доллар, Фунт.

- От Елена Кожухова

- • 06 окт. 2023 г. •

Российский фондовый рынок на следующей неделе может не показать значительных изменений, продолжая торговлю недалеко от текущих значений в отсутствие значимых драйверов движения.

- От Виктор Паньков

- • 05 окт. 2023 г. •

Вашему вниманию предоставляется математический анализ валютных инструментов S&P 500, EUR/USD, GBP/USD, USD/CAD, USD/JPY, USD/CHF, AUD/USD, NZD/USD, GOLD, BRENT, BTC/USD с.

How BlackRock’s S&P 500 UCITS ETF got tokenised

BlackRock founder and CEO Larry Fink’s vision that the “next generation for securities” would be tokenisation perhaps materialised faster than expected when his firm’s S&P 500 ETF was tokenised less than three months later by a Swiss start-up.

In February, structured product specialist Backed Finance entered the market with the Backed CSPX Core S&P 500 (bCSPX), a first-of-a-kind product on the ethereum blockchain tracking an ETF as an ERC-20 token.

This kind of token is a fungible smart contract offering access or representing the value of an asset; in this case Europe’s largest ETF, the iShares Core S&P 500 UCITS ETF (CSPX).

Backed Finance issues bCSPX from Switzerland and said it is backed by collateral in the form of the underlying asset on a 1:1 basis held by a licenced custodian. However, token-holders do not own the underlying and therefore do not have the right to company votes or dividends, as is the case with other derivative products.

Launching the product, the firm said: “Backed has spent the last two years building the new standard for compliant, fully collateralised, freely transferable tokenized real-world assets.

“We believe tokenisation will unlock trillions of dollars’ worth of value and power a new wave of economic activity.”

After years of crypto exchange-traded products (ETP) launches dominating headlines in Europe, the arrival of a tokenised ETF as a structural opposite illustrates how the wrapper is not only a tool for accessing new markets, but potentially also a tool for new markets to access conventional asset classes.

Marc-Thomas Arjoon, research associate at CoinShares, said: “I am a big proponent of the S&P 500 ETFs as most professional investment managers cannot outperform them in the long term. Giving the ability for anyone with an internet connection to be able to diversify their investments and gain exposure to the best performing stock market in the world is something I am a fan of.”

Laurent Kssis, crypto ETP specialist at CEC Capital, agreed, adding: “With tokenisation, I could be an investor in Vietnam trading in New Zealand assets 24 hours a day.

“Opening up that liquidity would make a palpable impact. The question is how regulation is going to protect investors regarding whether what these tokens say they do is actually what they hold.”

Access with limitations

However, as with any innovation, their selling points often require disclaimers. First, Backed Finance initially seeded enough liquidity to begin trading bCSPX using a pool on the Uniswap protocol, but the token is now unsupported by Uniswap due to potential legal reasons surrounding trading of the product.

The token also raises several red flags from a US regulatory perspective, such as offering permissionless access to US stocks via smart contracts, while simultaneously not being registered under the 1933 US Securities Act.

Sean Tuffy, former head of market and regulatory intelligence, custody and fund services at Citi, told ETF Stream: “Obviously, this will not be sold in the US because it would definitely qualify as a security offering. Ignoring the crypto magic, it is basically a derivative instrument.”

Kssis added: “The Securities and Exchange Commission is very harsh on this as they feel a lot of crypto issuance falls under securities and therefore, they want them to register and abide and comply with the regulatory regime.”

Thankfully, bCSPX has a better regulatory standing in Europe as it is issued under the Swiss Distributed Ledger Technology (DLT) Act and was also approved by the Financial Market Authority of Luxembourg, providing a window to European distribution.

Shane Coveney, partner at Dillon Eustace, said: “The ability to tokenise securities is still in the early phase of acceptance from a regulatory and legislative perspective.

“In Germany, for instance, as I understand it, the Electronic Securities Act (eWPG) was enacted which permits the issuing of electronic securities. However, there is no equivalent legislative basis in many other European jurisdictions.”

Outside of Europe, the scope for tokenised access is also limited, with Backed Finance noting it cannot service clients in Canada, Japan, a number of Latin American countries and all but two African states.

Structural risk or turning point?

Also, given its crypto DNA, bCSPX is potentially a haphazard way to gain exposure to ETFs.

Coveney added: “There are many risks including regulatory risks, technology risks – access to blockchain, change in protocols and investor loss of wallet key access, liquidity risks and counterparty risks.”

For now, Backed Finance’s prospectus notes the firm is unregulated and its products are not authorised by the Swiss Financial Market Supervisory Authority (FINMA), meaning they are exposed to the credit risk of the issuer – an unwelcome prospect following the collapse of crypto exchanges, lenders and custodians last year.

The prospectus added blockchain transaction costs, such as validator fees or gas costs, during periods of low volume or congestion may “substantially reduce” or have an “adverse impact” on the value of investments, with the issuer having “no ability to control or predict” these fees.

Finally, Tuffy questioned the mechanics of interfacing the token with the ETF to ensure it remained ‘fully backed’ on a 1:1 basis.

On this, the group’s prospectus conceded its ability to maintain collateral coverage is limited to the trading hours of its underlying, meaning its token may continue trading, unbacked, as the market for the underlying ETF is closed.

It also identified potential causes of tracking error, such as market or settlement disruption prompting the firm to postpone the valuation of its token. Also, potential illiquidity could have a “negative effect” on bCSPX’s price.

Despite these potential areas of friction, many remain positive about the prospects of tokenised assets. For Backed Finance, its S&P 500 ETF tracker may be just the first of many tokens it offers on publicly traded securities.

CEC Capital’s Kssis sees tokenisation offering fractionalisation opportunities beyond just conventional assets but noted in ETFs alone, collateralised tokens could offer a new source of liquidity for the wrapper.

This article first appeared in ETF Insider, ETF Stream's monthly ETF magazine for professional investors in Europe. To access the full issue, click here.

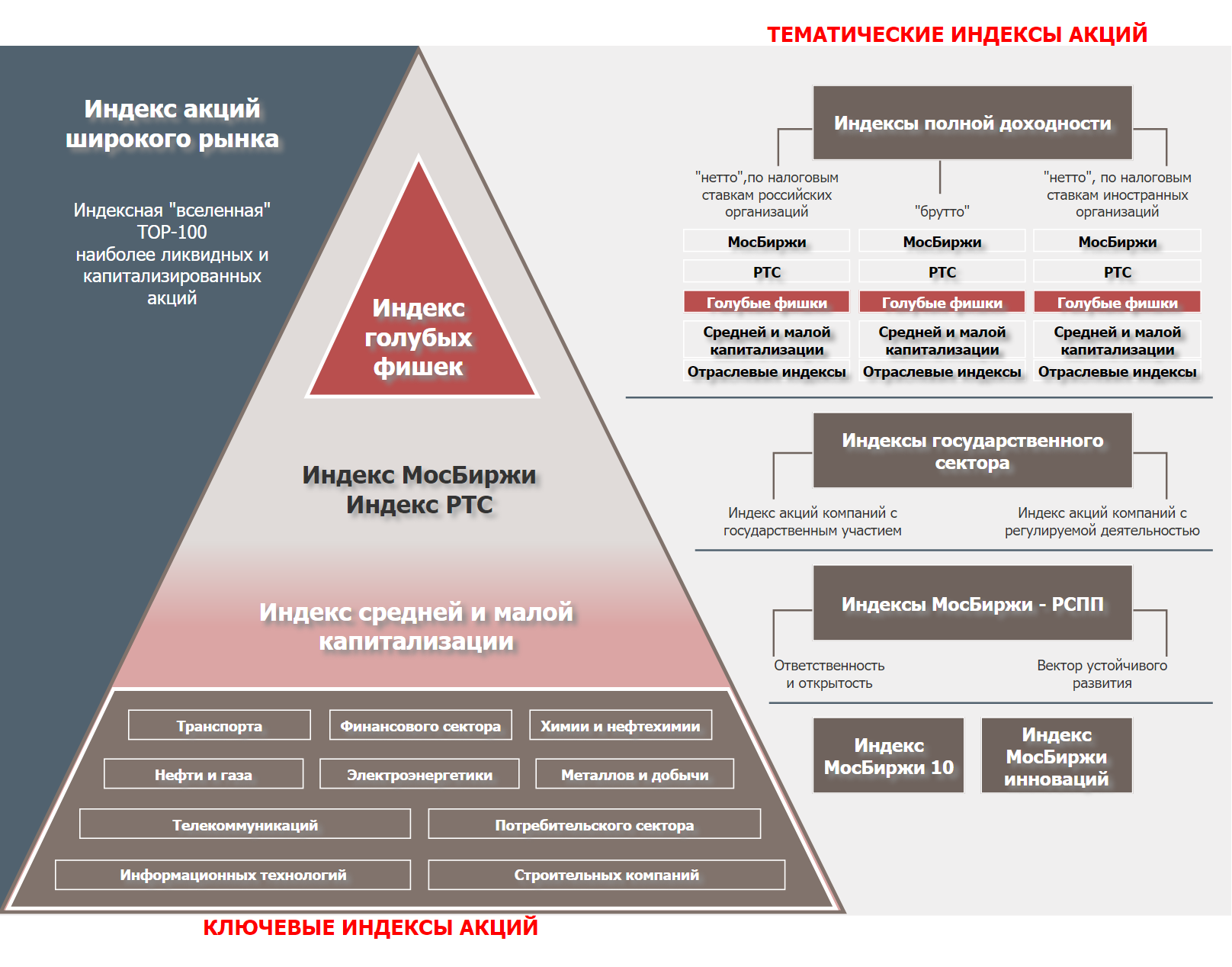

Что такое фондовые индексы

Биржевой индекс — это виртуальный набор активов, собранный по какому-то признаку. Чаще всего это ценные бумаги, но могут быть и биржевые товары.

Например, индекс может состоять из российских облигаций федерального займа, или из акций технологических компаний США, или из сельскохозяйственной продукции и сырья.

Разберу, зачем нужны индексы, какие они бывают и как в них инвестировать.

Зачем нужны индексы и откуда они берутся

Индексы помогают отслеживать поведение рынка ценных бумаг или иных активов. Это точнее и нагляднее, чем смотреть на поведение отдельных бумаг.

Как и цена акций и иных активов, значение индекса меняется много раз за день. Например, некий индекс состоит из акций крупных компаний США. Часть бумаг за день дорожает, часть — дешевеет, а цена некоторых не меняется.

Индекс меняется в соответствии со средневзвешенным изменением цены акций — с учетом доли, то есть веса, каждой акции в индексе. В итоге становится понятно, насколько в среднем вырос или упал рынок.

Индексы также помогают понять, как рынки вели себя в прошлом. Можно оценить доходность за много лет, величину просадок, волатильность, результаты лучших и худших лет и другие параметры.

Индексы рассчитывают компании-провайдеры или биржи. Они могут создать индекс по своей инициативе или рассчитывать его по заказу каких-то инвестиционных компаний, чтобы те могли создать на его основе фонды. О фондах мы еще поговорим.

Периодически состав индексов меняется: если какие-то активы перестали соответствовать требованиям индекса, их заменят на другие. Такое возможно, например, если доля акций в свободном обращении упала ниже допустимой. Пересмотр и ребалансировка индекса обычно проходят по расписанию: например, раз в полгода или квартал.

Какие бывают индексы

Индексов много — сотни и тысячи. Их можно классифицировать по многим параметрам. Назову основные.

По виду активов. Индексы акций состоят из акций, то есть долей в компаниях. Акции — довольно рискованный актив, так что такие индексы волатильны: их доходность сложно предсказать, а значение за день может вырасти или упасть на несколько процентов.

Индексы облигаций отслеживают состояние долгового рынка. Обычно такие индексы колеблются меньше, чем индексы акций, но и доходность в долгосрочной перспективе в среднем ниже.

Индексы биржевых товаров, или commodity, отслеживают, как меняется цена набора какого-то сырья или сельскохозяйственной продукции. Например, в индексе Bloomberg Commodity есть нефть, газ, золото, пшеница, соя, сахар и еще почти 20 позиций.

Есть также индексы денежного рынка, индексы волатильности и даже криптовалютные индексы.

По широте охвата или уровню диверсификации. Индексы могут отслеживать состояние какого-то небольшого набора бумаг по сектору, типу или географической принадлежности.

Например, существует индекс акций российских строительных компаний, в котором бумаги всего четырех компаний. Есть индекс FTSE Actuaries UK Index Linked Gilts Over 5 Years — индекс гособлигаций Великобритании с привязкой к инфляции, до погашения которых более пяти лет.

Есть и куда более диверсифицированные индексы, которые охватывают весь рынок какой-то страны, региона или всего мира. Туда входят сотни и даже тысячи бумаг.

Например, в индексе MSCI AC Asia ex Japan есть акции двух развитых и девяти развивающихся стран Азии, при этом оттуда исключена Япония. В индекс FTSE Global All Cap входят акции более 9000 компаний из почти 50 стран мира.

По способу формирования. Различия в том, как формируются индексы, удобно показать на примере индексов акций. Они часто взвешены по капитализации: доля бумаги в индексе такая же , как доля бумаги в капитализации рынка. Например, акции Apple имеют наибольший вес в S&P 500 — индексе акций крупных компаний США, потому что Apple — самая дорогая компания в США.

Может учитываться не только капитализация, но и доля акций в свободном обращении — так называемый коэффициент фри-флоат. Этот параметр применяется в том же S&P 500 и индексе Московской биржи.

Еще может искусственно ограничиваться максимальный вес одной бумаги. Так, в индексе Московской биржи доля акций одной компании не может превышать 15% на момент формирования базы расчета индекса, а в остальное время не может превышать 30%. Топ-5 составляющих не могут занимать более 55 и 60% индекса соответственно.

Взвешивание по капитализации удобно тем, что не надо постоянно корректировать состав индекса. Акции подорожали, из-за чего выросла капитализация компании — и автоматически выросла доля акции в индексе.

Бывают индексы, в которых все бумаги имеют равный вес. По сравнению с индексами, основанными на капитализации, такой подход снижает вес крупнейших компаний и увеличивает вес небольших. Равновзвешенные индексы надо периодически ребалансировать, даже если их состав не изменился.

Может быть и так, что самые дорогие компании занимают меньшую часть индекса. Это как взвешивание по капитализации, но наоборот. Такой подход встречается редко.

Что касается индексов облигаций, то в них вес отдельных бумаг может быть одинаковым — по крайней мере, в начале или сразу после ребалансировки. Или вес бумаг может определяться суммой заимствований тех, кто выпустил облигации.

Может использоваться даже ВВП стран, если речь о государственных облигациях. Последний подход применяется в индексе Solactive GDP Weighted Global Government Bond.

По виду доходности. Ценовые индексы основаны на том, как изменилась цена какого-то актива, например акций или облигаций. Дивиденды и купоны, то есть выплаты по ценным бумагам, не учитываются.

Еще есть индексы полной доходности, или total return. Они учитывают не только изменение цены, но и дивиденды или купоны. Если инвестор хочет оценить доходность какого-то вида активов, особенно в долгосрочной перспективе, лучше смотреть на индекс полной доходности.

Индекс полной доходности может считаться как без учета налогов с купонов и дивидендов, так и с поправкой на налог.

Например, есть ценовой индекс Московской биржи — без учета дивидендов от акций. В дополнение к нему рассчитываются индексы полной доходности:

- «брутто» — без учета налогов с дивидендов;

- «нетто» — по налоговым ставкам иностранных организаций;

- «нетто» — по налоговым ставкам российских организаций.

Как вложиться в индекс

Купить долю в индексе нельзя, потому что индекс — это условное понятие. Но можно инвестировать на основе индекса.

Это легче, чем выбирать отдельные акции или облигации. А главное, благодаря диверсификации снижается риск: в индексе обычно много бумаг, так что проблемы или даже банкротство нескольких компаний не приведут к значительным убыткам.

Вот несколько способов инвестировать на основе индекса.

Повторить вручную. Можно купить все бумаги из нужного индекса пропорционально их весу в индексе. Проблема в том, что точное повторение индекса обычно требует довольно крупного капитала: миллионов рублей или даже долларов. Для примерного повторения хватит и меньшей суммы, но тогда может отличаться результат.

Кроме того, ручное повторение индекса не очень удобно из-за затрат времени на покупку и продажу десятков и сотен бумаг. Еще это может быть менее выгодно из-за налогов.

Использовать производные инструменты. Можно использовать фьючерсы и опционы на индекс, но это рискованный инструмент из-за встроенного плеча. Кроме того, такие инструменты плохо подходят для долгосрочных инвестиций, а еще фьючерсы и опционы есть не на все индексы.

Использовать структурные продукты. Так называют комбинацию финансовых инструментов, обычно облигаций и опционов, в оболочке одного. Доходность структурного продукта может зависеть от поведения акции, валюты, индекса или иного базового актива.

У структурных продуктов есть минусы. Например, то, что они могут дать лишь часть доходности базового актива. Кроме того, досрочное погашение такого продукта часто приводит к убытку, а еще есть зависимость от надежности компании, которая выпустила продукт. Для некоторых продуктов может требоваться статус квалифицированного инвестора.

Купить паи фонда. Оптимальный способ — купить долю в инвестиционном фонде, то есть в ETF или биржевом ПИФе, отслеживающем нужный вам индекс. Долю в фонде называют паем или акцией. В фонде содержатся бумаги из индекса в нужных пропорциях, и если у инвестора есть паи фонда, то у него есть кусочек всех активов.

Цена пая зависит от того, как меняется стоимость активов в фонде. Например, если фонд отслеживает индекс S&P 500 и акции в составе индекса и фонда в среднем выросли, цена пая увеличится. Если индекс падает, пай тоже будет дешеветь.

Фонд берет комиссию за управление. В зависимости от фонда это может быть от доли процента до нескольких процентов в год от стоимости активов. Комиссия постепенно списывается из активов фонда и автоматически учитывается в цене его паев.

Паи инвестиционных фондов можно купить и продать на бирже так же , как обычные акции. Некоторые фонды платят дивиденды, некоторые — нет.

Через российских брокеров можно совершать сделки с ETF и БПИФами на Московской бирже. Через них же можно получить доступ к фондам на иностранных биржах, но понадобится статус квалифицированного инвестора.

Торговать на иностранных биржах можно и через иностранного брокера, например американского Interactive Brokers. Статус квалифицированного инвестора в таком случае не нужен, еще будет доступно больше фондов и других активов. Но придется самому считать доходы и платить налоги, а также сообщать в налоговую об открытии и закрытии счета и о движении средств.

Cspx и csspx в чем отличие

@1: So this form lets you get the American tax back. Do they always give back everything? You just fill it out?

@2: So if I buy an Ireland-domiciled ETF, Ireland will put a withholding tax on my dividends? And not Switzerland? There will be no double taxation? And is there a way to get the tax back from Ireland?

@3: You mean earnings from the stock market or salary? Because who earns 25k from salary? And why only a half back?

@1: So this form lets you get the American tax back. Do they always give back everything? You just fill it out?

@2: So if I buy an Ireland-domiciled ETF, Ireland will put a withholding tax on my dividends? And not Switzerland? There will be no double taxation? And is there a way to get the tax back from Ireland?

@3: You mean earnings from the stock market or salary? Because who earns 25k from salary? And why only a half back?

1) no the form allows for reduced withholding tax of 15%. Put it on a tax return for refund.

2) Switzerland has no control on anything in Ireland, UNLESS it’s HELD by a Swiss institution.

3) Total taxable income, you need to look at the exact salary range where full withholding tax is not refunded. Because thats what they choose to do.

In Malta I only get full withholding tax credit if my local tax rate averages 15% or more.

Like, on a Swiss tax return form? An American tax?

"Held" meaning the broker? So if you keep Irish ETF by a Swiss broker, then what happens?

3) Total taxable income, you need to look at the exact salary range where full withholding tax is not refunded. Because thats what they choose to do.

In Malta I only get full withholding tax credit if my local tax rate averages 15% or more.

And now comes Malta to confuse me even more . What is your relation with Malta?

What I’m trying to find out is pretty straightforward: Earning in CHF in Switzerland, in which country and in which currency should I keep my ETF’s to minimize taxes, costs and paperwork?

Like, on a Swiss tax return form? An American tax?

"Held" meaning the broker? So if you keep Irish ETF by a Swiss broker, then what happens?

And now comes Malta to confuse me even more . What is your relation with Malta?

What I’m trying to find out is pretty straightforward: Earning in CHF in Switzerland, in which country and in which currency should I keep my ETF’s to minimize taxes, costs and paperwork?

Yes a Swiss tax return

Held means the broker, a Swiss broker will withhold 30% for US withholding tax

I am now tax resident in Malta, where I am only liable to tax on income EARNEN or REMITTED to Malta, not world wide income or world wide capital gains although all gains can be remitted to Malta free of tax. The sun shines 300 days a year, the national language includes English, 13 amp plugs on the wall & the concept of shared washing machines does not exist.. When the snow falls I ski in Verbier & Chamonix for the winter.

That’s a cool retirement spot. I will add it to my shortlist. The concept of shared washing machines is something I can’t get over. Where I come from it is also unheard of, even though it’s a far poorer country that Switzerland. I’m so used to it that I had to find an apartment that has a washing machine. And it always makes me laugh when I hear "I can’t come today, because it’s my laundry day on the schedule".

So getting back to the topic, what simple low-cost buy and hold arrangement would you recommend to a Swiss earner?

That’s a cool retirement spot. I will add it to my shortlist. The concept of shared washing machines is something I can’t get over. Where I come from it is also unheard of, even though it’s a far poorer country that Switzerland. I’m so used to it that I had to find an apartment that has a washing machine. And it always makes me laugh when I hear "I can’t come today, because it’s my laundry day on the schedule".

So getting back to the topic, what simple low-cost buy and hold arrangement would you recommend to a Swiss earner?

Charles Schwab or any low cost US broker

- A Swiss domiciled investor buys iShares Core S&P 500 UCITS ETF (CSSPX) with a Swiss broker. The ETF is domiciled in Ireland and traded on the Swiss Exchange.

- A Swiss domiciled investor buys iShares Core S&P 500 UCITS ETF (CSPX) with an Irish broker. The ETF is domiciled in Ireland and traded on the London Exchange.

- A Swiss domiciled investor buys iShares Core S&P 500 ETF (IVV) with an American broker. The ETF is domiciled in USA and traded on the New York Exchange.

- In case of dividend payout, what will be the withholding tax in each case?

- What decides which country’s tax has to be paid? Is it the domicile of the fund, the trading place, or the investor?

- In each case, is it possible to get a refund of the tax?

- Does it make a difference if you buy an accumulating or distributing ETF?

Stamp duty is not levied on ETF trades directly, rather the ETF ask price will reflect the stamp duty cost associated with buying the components of the ETF which attract the stamp duty fee.

So in this sense Irish domiciled ETFs make no difference in that sense.

I’d have to check further but the major domicile centres of most European ETFs are: Ireland, Luxembourg, Switzerland, France and Germany. It would be interesting to see a comparison table to see how these domicile countries compare in terms of tax efficiency but my guess is that they are all fairly similar.

Stamp duty is not levied on ETF trades directly, rather the ETF ask price will reflect the stamp duty cost associated with buying the components of the ETF which attract the stamp duty fee.

So in this sense Irish domiciled ETFs make no difference in that sense.

I’d have to check further but the major domicile centres of most European ETFs are: Ireland, Luxembourg, Switzerland, France and Germany. It would be interesting to see a comparison table to see how these domicile countries compare in terms of tax efficiency but my guess is that they are all fairly similar.

An EFT is traded on the open market, not bought & sold by the fund manager once a day so I am not convinced your correct.

EDIT, Irish EFT’s are exempt from stamp duty when traded on the LSE.

A simple test would be to buy an ETF domiciled in Ireland and test to see if any stamp duty is levied. I can provide some examples from different issuers, maybe someone who traded these ETFs can confirm for sure.

I think it really doesn’t matter where they are traded.

So as an extension to my simple test above, we might have to test buying / asking the different exchanges whether they levy any stamp duty on ETFs. I am not aware of any that do. (Maybe Swiss Stock Exchange, levies some transaction tax on ETFs? not sure)

Found the following documents on Irish domiciled ETFs which might be useful as a future reference:

Ireland�s attractiveness as an ETF domicile is due to several factors, including Ireland�s extensive network of tax treaties with key jurisdictions worldwide which enables ETFs to access the double taxation treaties where the fund is demonstrated to be trading. In particular, Irish ETF�s can benefit from the USA/Ireland double tax treaty which reduces withholding tax to zero on interest and 15% on dividends.

Irish funds, including ETFs, are not subject to Irish taxation on any income or gains realised from underlying investments.

They are also exempt from withholding tax. Similarly, no stamp duty regarding shares in an ETF, or on the underlying shares it holds (as long as those underlying shares are not issued by an Irish registered company, do not relate to Irish property). ETFs can also enjoy beneficial VAT exemptions.

A rehash of the same info from irishfunds.ie

Another piece of information is regarding the VCC (Variable Capital Company) structure which a lot of these ETFs are set up as in Ireland.

And finally a note on the ICAV (Irish Corporate Asset-management Vehicle) structure which is supposed to cater specifically for funds.

A lot of the information in these documents is a bit of an over kill for a retail investor, and will probably make very little difference in the end as the ETF issuers will change the fund structures to take advantage of the latest tax efficiencies etc.